Introduction

Unsecured credit cards have become one of the most accessible financial tools for building credit and managing everyday expenses in 2026. Unlike secured credit cards that require a cash deposit, unsecured cards offer credit based solely on your creditworthiness. This comprehensive guide explains everything beginners need to know about unsecured credit cards, including how they work, their benefits, potential drawbacks, and how to choose the right card for your financial situation.

Whether you’re looking to build your credit history, earn rewards on purchases, or consolidate existing debt, understanding unsecured credit cards is essential. This guide will help you make informed decisions about credit card selection and usage to maximize benefits while minimizing risks.

What Are Unsecured Credit Cards?

An unsecured credit card is a type of credit card that doesn’t require you to provide a cash deposit or collateral to open an account. Instead, the card issuer extends credit based on your creditworthiness, which is determined by factors such as your credit score, income, employment history, and existing debt. This is different from secured credit cards, which require a deposit equal to your credit limit.

When you use an unsecured credit card, you’re essentially borrowing money from the card issuer. You’re required to pay back the borrowed amount, either in full or in monthly installments. If you don’t pay the full balance, you’ll be charged interest on the remaining balance at the card’s Annual Percentage Rate (APR).

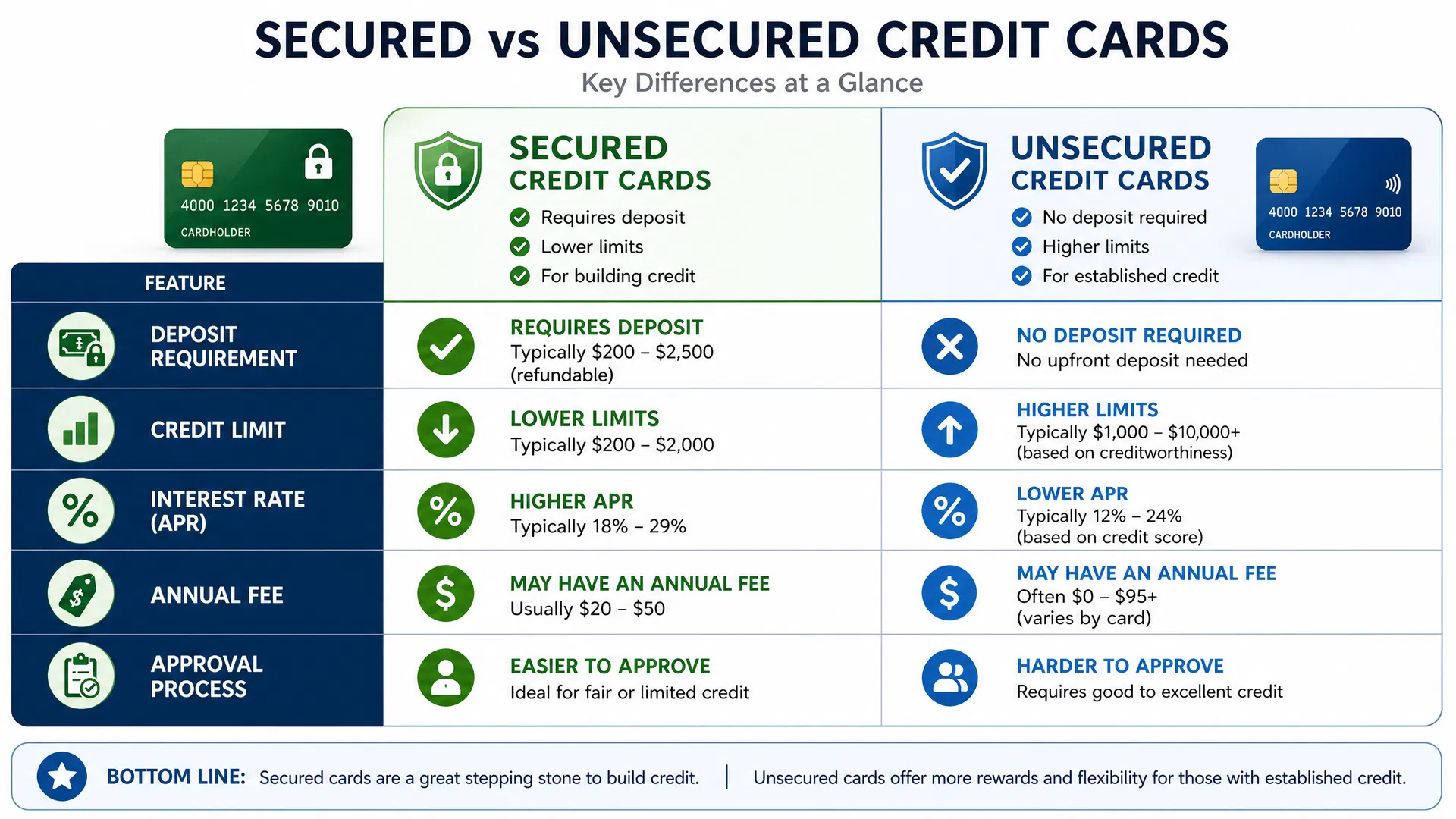

Secured vs. Unsecured Credit Cards

Understanding the differences between secured and unsecured credit cards is crucial for beginners. Secured cards require a cash deposit (typically $200-$2,500) that serves as collateral. This deposit equals your credit limit, making it easier for banks to approve applications. Unsecured cards, on the other hand, don’t require any deposit and are based entirely on your creditworthiness.

Secured cards are ideal for people building credit from scratch or recovering from poor credit history. They’re easier to qualify for and help establish a positive payment history. Unsecured cards offer higher credit limits, better rewards programs, and more flexibility. However, they require good to excellent credit for approval.

| Feature | Secured Cards | Unsecured Cards |

|---|---|---|

| Deposit Required | Yes ($200-$2,500) | No |

| Credit Limit | $200-$2,000 (typically) | $1,000-$10,000+ (varies) |

| Typical APR | 18%-29% | 12%-24% |

| Annual Fee | $0-$50 | $0-$95+ |

| Rewards | Limited or none | Cashback, points, miles |

| Best For | Building credit | Established credit |

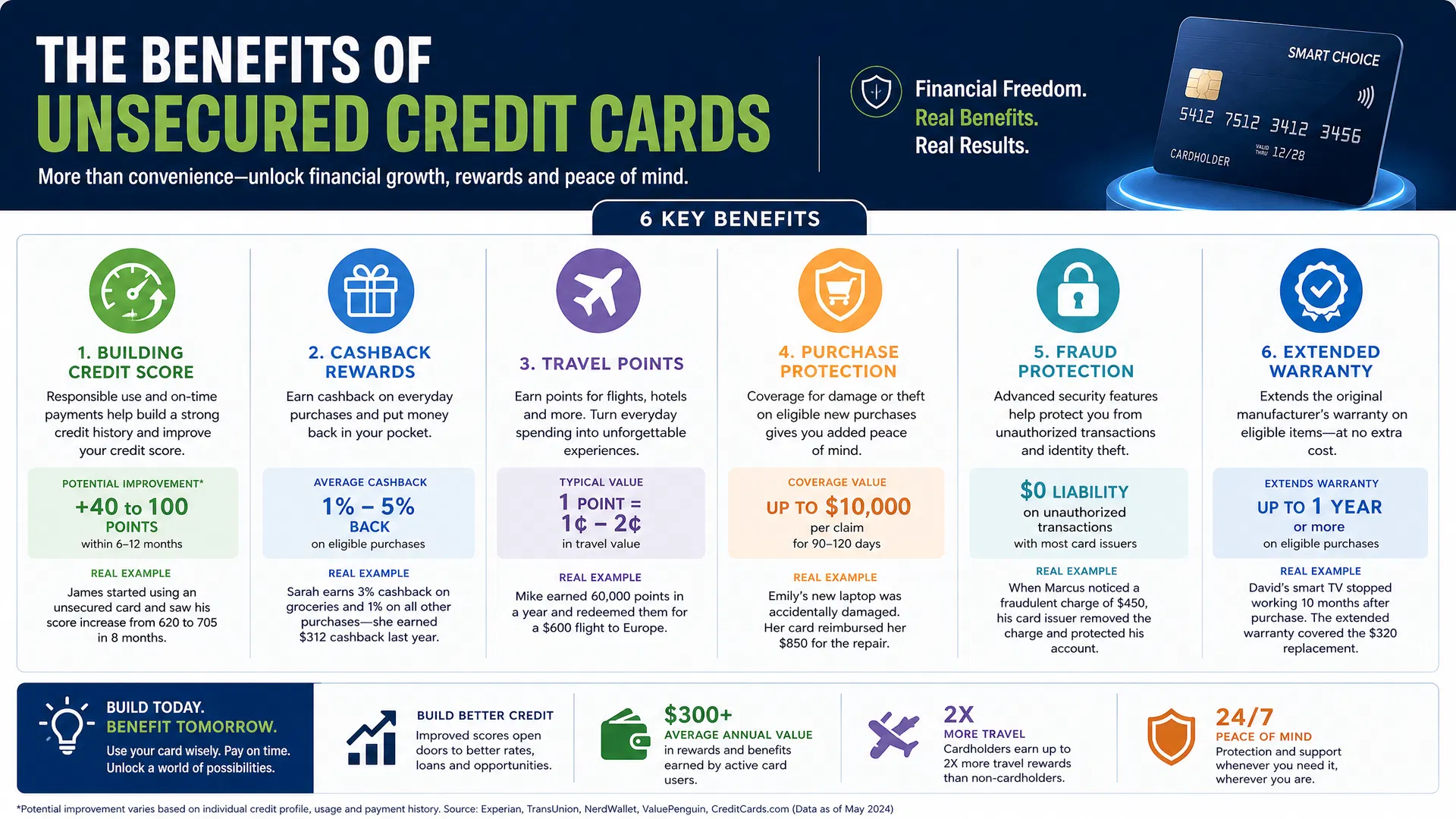

Benefits of Unsecured Credit Cards

1. Building and Improving Credit Score

One of the most significant benefits of unsecured credit cards is their ability to help you build or improve your credit score. When you use a credit card responsibly and make on-time payments, this positive payment history is reported to credit bureaus. Over time, consistent responsible use can increase your credit score by 40-100 points or more, opening doors to better interest rates on loans and mortgages.

2. Earning Rewards

Most unsecured credit cards offer reward programs that allow you to earn cashback, points, or travel miles on your purchases. Depending on the card, you might earn 1-5% cashback on eligible purchases. This means you can earn money back on everyday spending like groceries, gas, and dining. Some cards offer bonus categories with higher rewards rates.

3. Purchase Protection and Fraud Prevention

Unsecured credit cards typically include purchase protection that covers damage or theft of items purchased with the card. Many cards also offer extended warranty coverage, price protection, and return protection. Additionally, credit cards provide $0 liability for unauthorized transactions, protecting you from fraud.

4. Travel Benefits

Travel rewards credit cards offer benefits like free travel insurance, airport lounge access, and travel credits. Frequent travelers can earn enough points or miles to cover flights, hotels, and other travel expenses, making vacations more affordable.

5. Financial Flexibility

Unsecured credit cards provide financial flexibility by allowing you to make purchases even when you don’t have cash immediately available. This can be helpful for emergencies or planned expenses. However, it’s important to use this flexibility responsibly to avoid accumulating excessive debt.

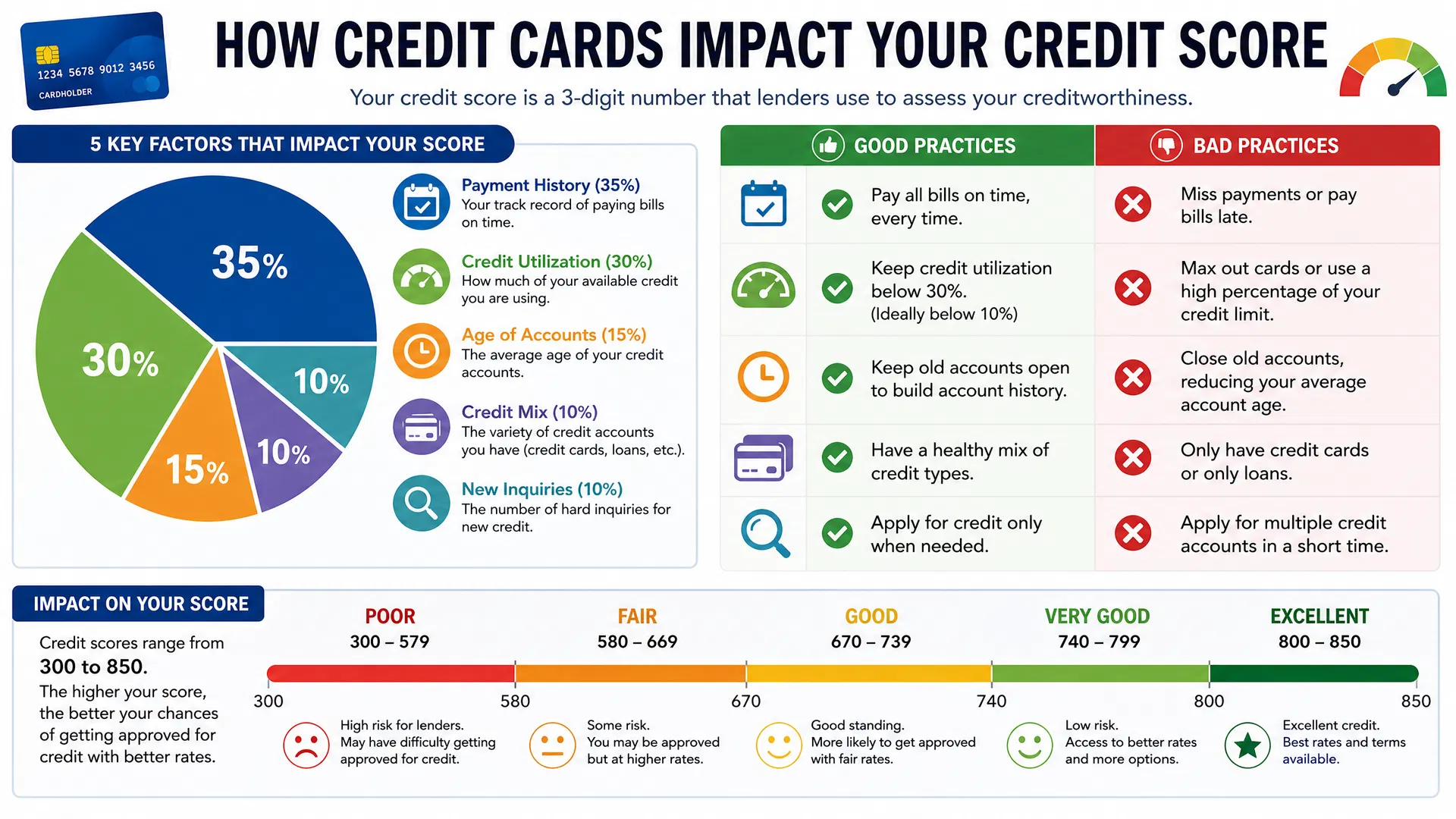

How Credit Cards Impact Your Credit Score

Your credit score is calculated based on five key factors. Payment history (35%) is the most important—always paying your bills on time significantly boosts your score. Credit utilization (30%) measures how much of your available credit you’re using. Keeping utilization below 30% (ideally below 10%) is ideal. Age of accounts (15%) rewards you for maintaining older accounts. Credit mix (10%) considers the variety of credit types you have. New inquiries (10%) reflect recent credit applications.

To maximize your credit score with unsecured credit cards, pay all bills on time, keep your credit utilization low, maintain old accounts, and avoid applying for multiple cards in a short period.

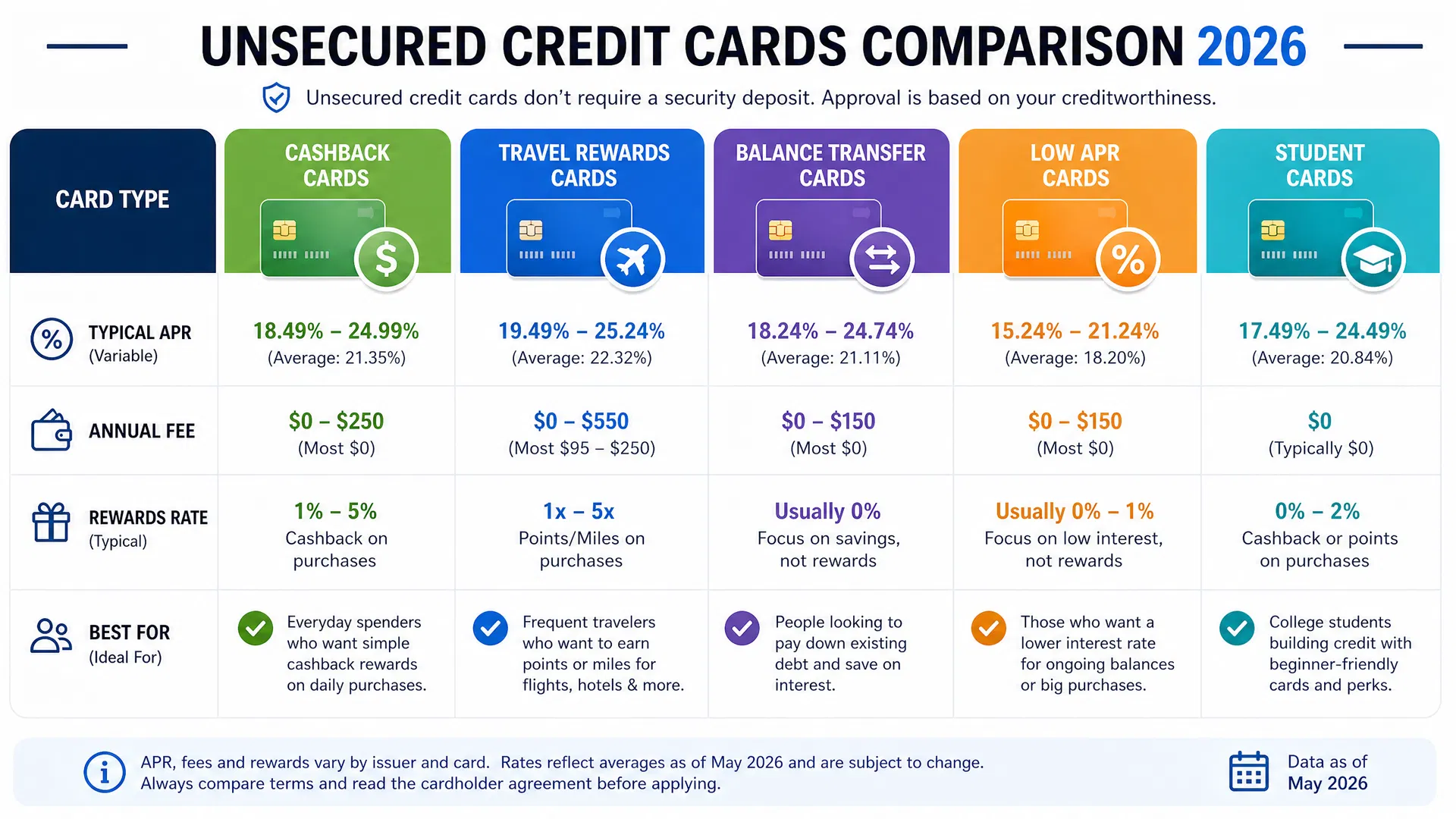

Types of Unsecured Credit Cards in 2026

Cashback Cards

Cashback cards return a percentage of your spending back to you as cash. Most cashback cards offer 1-5% cashback on purchases, with higher rates in specific categories like groceries, gas, or dining. These cards are ideal for everyday spenders who want simple, straightforward rewards.

Travel Rewards Cards

Travel rewards cards earn points or miles on purchases that can be redeemed for flights, hotel stays, and other travel expenses. Frequent travelers can accumulate significant value, potentially earning free trips. Many travel cards also offer travel insurance and airport lounge access.

Balance Transfer Cards

Balance transfer cards offer low or 0% APR for a promotional period (typically 6-21 months) on transferred balances. These cards are designed for people looking to consolidate existing credit card debt and pay it down during the promotional period. Learn more about debt consolidation strategies to maximize your savings.

Low APR Cards

Low APR cards offer reduced interest rates on purchases and balance transfers, making them ideal for people who carry balances. While they may not offer generous rewards, the lower interest rates can save significant money over time.

Student Credit Cards

Student cards are designed for college students with limited credit history. They typically have lower credit limits and may offer student-specific rewards. These cards help students build credit while in school, preparing them for better cards after graduation.

How to Choose the Right Unsecured Credit Card

1. Assess Your Credit Score

Your credit score determines which cards you can qualify for. Excellent credit (750+) opens access to premium cards with high rewards. Good credit (700-749) qualifies for solid mid-tier cards. Fair credit (650-699) may limit options to cards with lower rewards. Poor credit (below 650) may require a secured card first.

2. Determine Your Spending Patterns

Consider where you spend most of your money. If you travel frequently, a travel rewards card makes sense. If you spend heavily on groceries and gas, a cashback card with bonus categories is better. If you carry balances, a low APR card is most important.

3. Compare APR and Fees

Look at the card’s Annual Percentage Rate (APR) and any annual fees. A card with a $95 annual fee might still be worth it if you earn enough rewards to offset it. Compare the total cost of ownership, not just the APR or fee alone.

4. Review Rewards Programs

Evaluate the rewards structure carefully. Some cards offer flat-rate rewards (1% on all purchases), while others offer bonus categories. Calculate your potential annual rewards based on your spending patterns.

5. Check for Additional Benefits

Look beyond rewards for additional benefits like purchase protection, extended warranty, travel insurance, and fraud protection. These benefits add real value, especially for frequent travelers or large purchasers.

Best Practices for Using Unsecured Credit Cards

- Pay your full balance on time every month to avoid interest charges and build excellent credit

- Keep your credit utilization below 30% of your available credit limit

- Don’t close old credit card accounts, as this reduces your average account age

- Monitor your credit report regularly for errors or fraudulent activity

- Set up automatic payments to ensure you never miss a due date

- Avoid applying for multiple cards in a short time period

- Use your card for planned purchases, not impulsive ones

- Take advantage of sign-up bonuses by meeting spending requirements responsibly

- Review your statements monthly for unauthorized charges

- Keep your card information secure and never share your PIN or CVV

Common Mistakes Beginners Make

Many beginners make costly mistakes with unsecured credit cards. The most common mistake is carrying a balance and paying interest. Even a small balance at high APR can cost hundreds annually. Another mistake is maxing out credit limits, which damages your credit score and makes debt difficult to manage. Applying for too many cards at once triggers multiple hard inquiries, temporarily lowering your score. Missing payments is perhaps the worst mistake, as it severely damages credit and may result in late fees and higher APR.

To avoid these mistakes, treat your credit card as a tool for building credit and earning rewards, not as free money. Spend only what you can afford to pay back in full each month.

Frequently Asked Questions (FAQs)

A: Most unsecured credit cards require a credit score of 700 or higher. However, some issuers offer cards for fair credit (650-699). If your score is below 650, you may need to start with a secured card first.

A: You can see credit score improvements within 3-6 months of responsible credit card use. However, building excellent credit typically takes 1-2 years of consistent on-time payments and low credit utilization.

A: APR (Annual Percentage Rate) includes the interest rate plus other costs and fees. The interest rate is just the cost of borrowing. For credit cards, APR and interest rate are often used interchangeably.

A: Always pay your full balance if possible. Paying only the minimum means you’ll pay significant interest charges over time. If you must carry a balance, pay as much as you can afford beyond the minimum.

A: Most experts recommend having 2-4 credit cards. Multiple cards help your credit mix and provide backup payment options. However, managing too many cards can lead to missed payments and overspending.

A: Yes, many issuers allow you to graduate from a secured card to an unsecured card after demonstrating responsible use (typically 6-12 months). Your deposit is returned when you upgrade.

A: If denied, ask the issuer for the reason. Common reasons include low credit score, insufficient income, or too many recent applications. Address the issue (improve credit score, increase income, wait before applying again) and try again later.

A: It depends on your spending. If you spend $10,000+ annually and earn 2% cashback, you’d earn $200, offsetting a $95 annual fee. Calculate your potential rewards before applying for fee-based cards.

People Also Asked Questions (PAA)

Common Questions People Search For

Unsecured credit cards work by allowing you to borrow money from the card issuer without providing collateral. You receive a credit limit based on your creditworthiness. When you make purchases, the amount is added to your balance. You must repay the balance monthly, either in full or in installments. If you carry a balance, you’re charged interest at the card’s APR.

Getting an unsecured card with bad credit is challenging but possible. Some issuers offer cards specifically for fair or poor credit, though they may have higher APR, annual fees, and lower credit limits. Alternatively, start with a secured card to rebuild credit, then graduate to an unsecured card after 6-12 months of responsible use.

If you don’t pay your credit card bill, you’ll face late fees (typically $25-$40), increased APR, and damage to your credit score. Missed payments stay on your credit report for 7 years. If you miss payments for 180+ days, the account may be charged off and sent to collections.

Request a credit limit you can manage responsibly. Most first-time applicants receive $500-$2,000. You can request a higher limit after demonstrating responsible use for 6-12 months. Remember, a higher limit doesn’t mean you should spend more—keep utilization low regardless of limit size.

Having multiple credit cards isn’t inherently bad—it can actually improve your credit mix and provide backup payment options. However, managing too many cards increases the risk of missed payments and overspending. Most experts recommend 2-4 cards for most people.

A credit card is right for you if: (1) You can qualify based on your credit score, (2) The rewards align with your spending patterns, (3) You can afford the annual fee (if any) through earned rewards, (4) You commit to paying your balance in full monthly, and (5) You need to build or maintain credit history.

The best card depends on your situation. For building credit: look for cards with no annual fee and cashback rewards. For travel: choose travel rewards cards with sign-up bonuses. For low APR: select balance transfer cards with 0% promotional rates. Compare options based on your specific needs and credit score.

Most issuers allow you to request a credit limit increase after 6 months of responsible use. You can request online, by phone, or through your account. Issuers may perform a hard inquiry (which temporarily lowers your score) or a soft inquiry (no impact). A higher limit can improve your credit utilization ratio if you don’t increase spending.

Important Considerations

Conclusion

Unsecured credit cards are powerful financial tools for beginners when used responsibly. They offer opportunities to build credit, earn rewards, and gain financial flexibility. However, they also carry risks if misused, including high interest charges and credit damage from missed payments.

The key to success with unsecured credit cards is understanding how they work, choosing the right card for your situation, and committing to responsible use. Pay your full balance monthly, keep your credit utilization low, and monitor your credit score regularly. By following these practices, you can build excellent credit while earning valuable rewards.

Remember, understanding different financial products like loans helps you make better overall financial decisions. Start your credit journey today with a card that matches your needs, and watch your financial future improve.

{kind=link}