Complete guide to loan types including personal loans, mortgages, auto loans, student loans, and more. Learn the pros and cons of each loan type for USA and UK borrowers.

When you need financial assistance, understanding the different types of loans available is crucial to making the right decision. Whether you’re in the United States or the United Kingdom, the lending landscape offers numerous options tailored to different financial situations and needs. This comprehensive guide explains the major loan types, their features, advantages, and disadvantages to help you choose the best option for your circumstances.

The loan market has evolved significantly over the past decade, with traditional banks now competing alongside online lenders, credit unions, and peer-to-peer platforms. Each loan type serves a specific purpose and comes with its own terms, interest rates, and requirements. Understanding these differences can save you thousands of dollars in interest payments and help you avoid predatory lending practices.

What Is a Loan?

A loan is a sum of money borrowed from a lender with the agreement to repay it with interest over a specified period. The interest rate represents the cost of borrowing and is typically expressed as an annual percentage rate (APR). Loans are fundamental financial tools that help individuals and businesses achieve their goals, whether purchasing a home, funding education, consolidating debt, or handling emergencies.

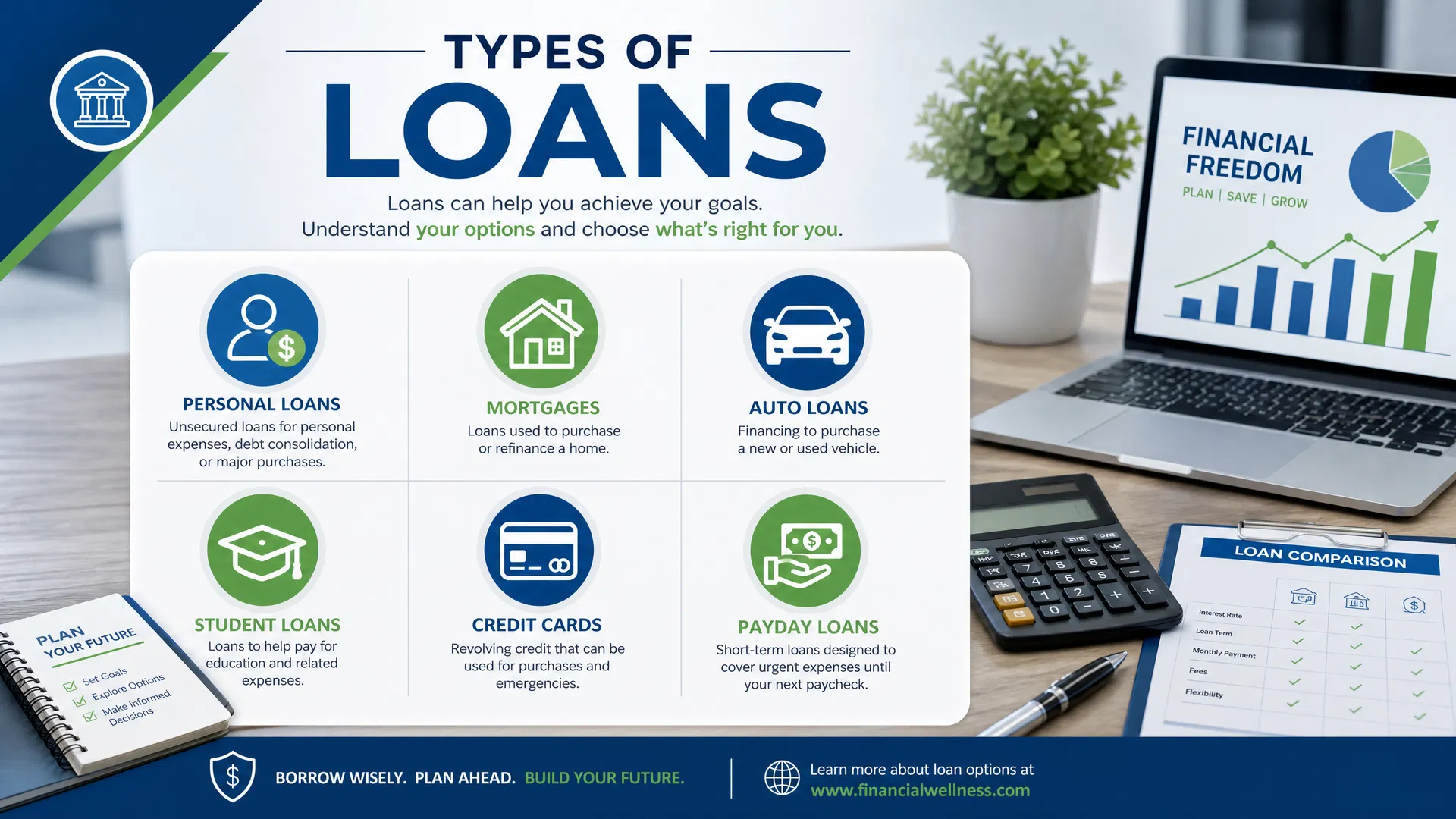

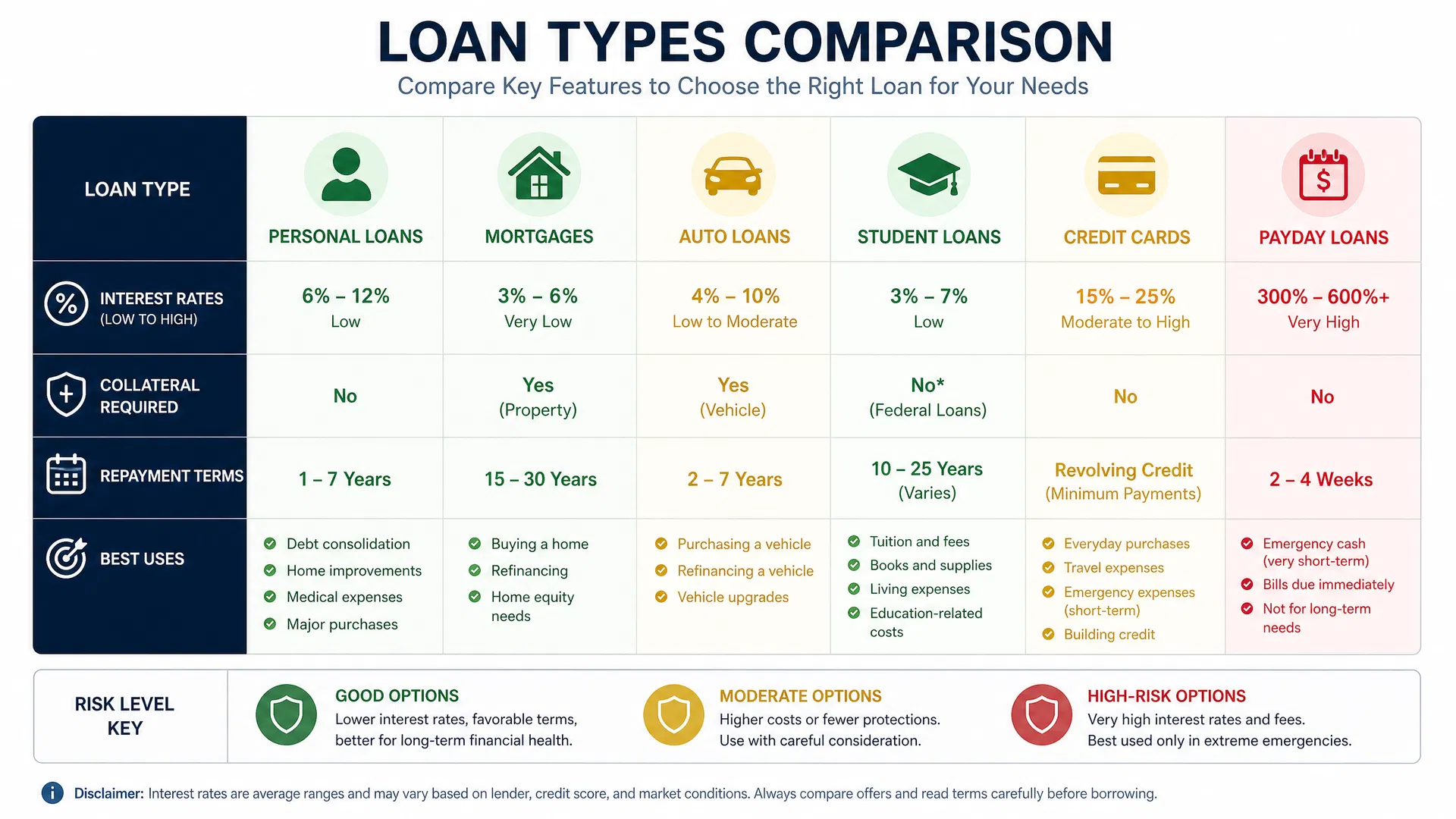

1. Personal Loans

Definition and Purpose

Personal loans are unsecured loans that can be used for virtually any purpose. Unlike secured loans, personal loans don’t require collateral, meaning the lender cannot seize your assets if you default. This makes them more accessible but typically comes with higher interest rates.

Key Features

- Unsecured (no collateral required)

- Fixed interest rates (usually)

- Fixed repayment terms (typically 2-7 years)

- Loan amounts typically range from $1,000 to $50,000 (USA) or £1,000 to £25,000 (UK)

- Quick approval process (often within 24-48 hours)

Best For

- Debt consolidation

- Home improvements

- Medical expenses

- Weddings

- Vacation expenses

- Emergency expenses

Advantages

- No collateral required

- Quick funding

- Flexible use of funds

- Predictable monthly payments

- Available from multiple lenders

Disadvantages

- Higher interest rates than secured loans

- Stricter credit requirements

- May require a co-signer for poor credit

- Origination fees may apply

Interest Rates

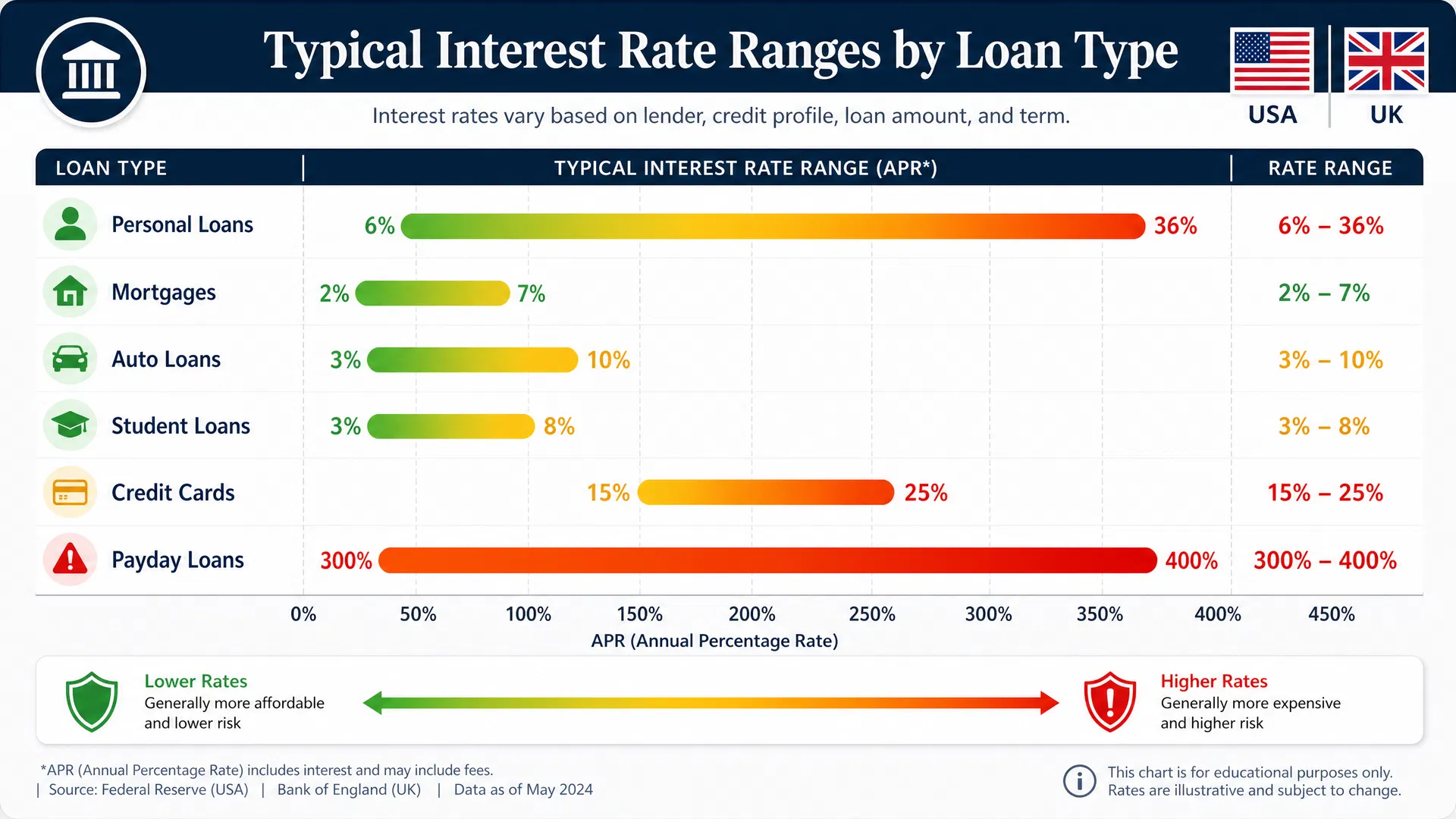

In the USA, personal loan rates typically range from 6% to 36% APR depending on creditworthiness. In the UK, rates generally range from 3% to 50% APR, with better rates for those with excellent credit scores.

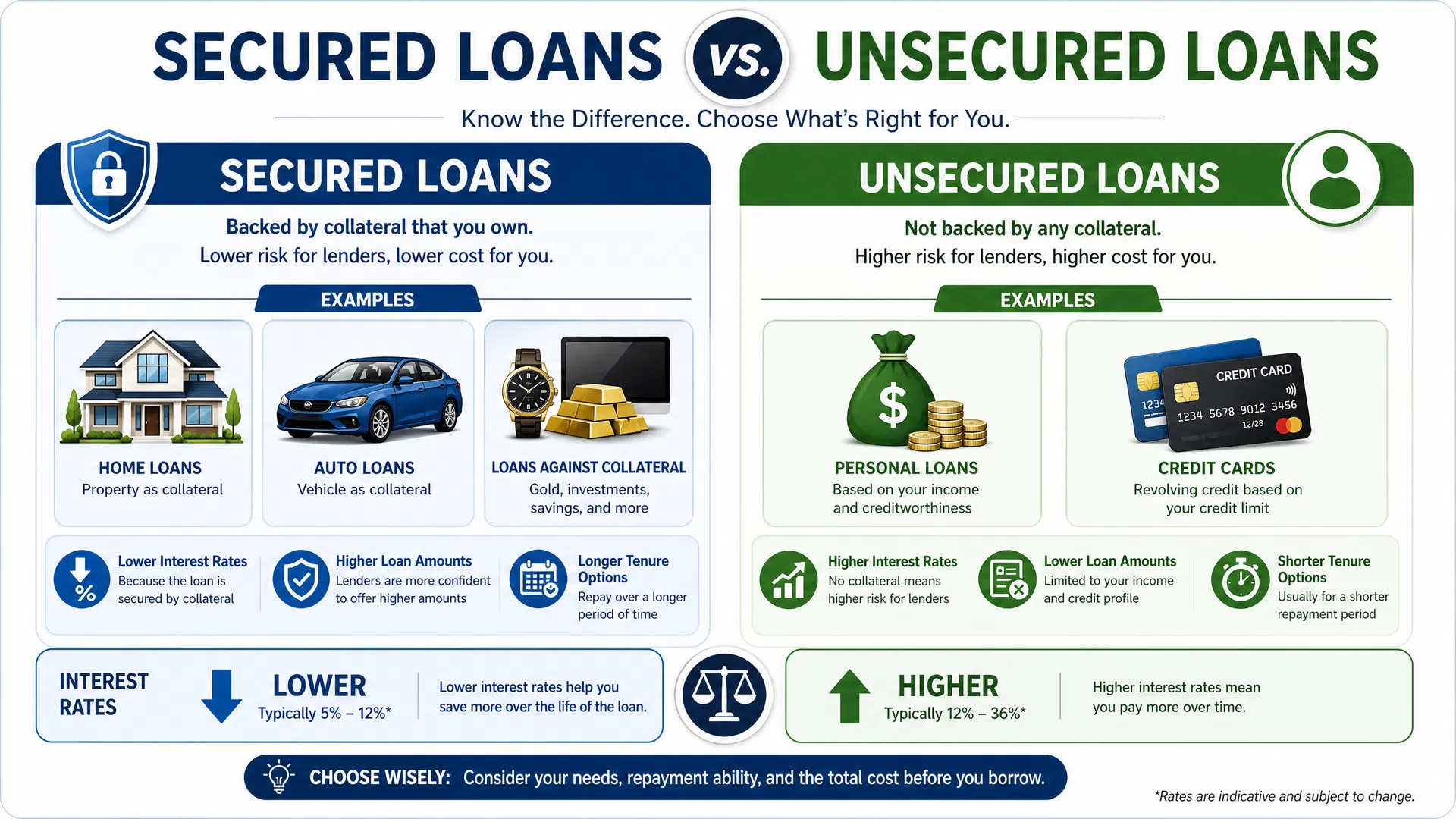

2. Secured Loans

Definition and Purpose

Secured loans require collateral—an asset of value that the lender can seize if you fail to repay. Common collateral includes vehicles, home equity, savings accounts, or other valuable assets. Because the lender has security, these loans typically offer lower interest rates.

Key Features

- Requires collateral

- Lower interest rates than unsecured loans

- Larger loan amounts possible

- Longer repayment terms available

- May be easier to qualify for with poor credit

Best For

- Home improvements

- Vehicle purchases

- Debt consolidation

- Large purchases

- Business funding

Advantages

- Lower interest rates

- Larger borrowing amounts

- Easier approval for poor credit

- Longer repayment periods

- More flexible terms

Disadvantages

- Risk of losing collateral

- More paperwork required

- Longer approval process

- Asset valuation required

- Prepayment penalties may apply

3. Mortgages

Definition and Purpose

Mortgages are long-term secured loans specifically designed for purchasing real estate. The property itself serves as collateral. Mortgages are the most common type of loan in both the USA and UK, with terms typically ranging from 15 to 30 years.

Types of Mortgages

Fixed-Rate Mortgages: Interest rate remains the same throughout the loan term. Offers predictability and protection against rising rates.

Adjustable-Rate Mortgages (ARMs): Interest rate changes periodically based on market conditions. Often starts with a lower rate but can increase significantly.

Interest-Only Mortgages: Borrower pays only interest for an initial period, then principal and interest. Riskier but offers lower initial payments.

Key Features

- Secured by the property

- Long repayment terms (15-30 years typically)

- Large loan amounts

- Lower interest rates compared to unsecured loans

- Strict qualification requirements

Advantages

- Lowest interest rates available

- Tax-deductible interest (in many cases)

- Builds home equity

- Long repayment period reduces monthly payments

- Wealth-building opportunity

Disadvantages

- Strict qualification requirements

- Risk of foreclosure

- Long approval process

- Large upfront costs (down payment, closing costs)

- Property appraisal required

4. Auto Loans

Definition and Purpose

Auto loans are secured loans specifically for purchasing vehicles. The vehicle serves as collateral, allowing lenders to offer competitive interest rates. Auto loans are available from banks, credit unions, dealerships, and online lenders.

Key Features

- Secured by the vehicle

- Typical terms: 3-7 years

- Loan amounts: $5,000 to $100,000+

- Vehicle must be insured

- Mileage and condition restrictions may apply

Best For

- Purchasing new vehicles

- Purchasing used vehicles

- Vehicle refinancing

Advantages

- Competitive interest rates

- Quick approval process

- Flexible terms

- Can build credit history

- Predictable monthly payments

Disadvantages

- Vehicle depreciates rapidly

- Risk of being “underwater” (owing more than vehicle worth)

- Mileage restrictions

- Insurance requirements

- Early payoff penalties may apply

Interest Rates

USA auto loan rates typically range from 3% to 10% APR. UK rates generally range from 2% to 15% APR, depending on credit score and vehicle type.

5. Student Loans

Definition and Purpose

Student loans are designed to help students pay for higher education expenses. They’re available from government agencies and private lenders. Student loans typically have lower interest rates and more flexible repayment options than other loan types.

Types of Student Loans

Federal Student Loans (USA): Offered by the government with fixed rates and income-driven repayment options.

Private Student Loans: Offered by banks and lenders with variable or fixed rates.

UK Student Loans: Offered by the government with repayment based on income.

Key Features

- Lower interest rates than personal loans

- Flexible repayment options

- Deferment and forbearance available

- May offer loan forgiveness programs

- No collateral required

Advantages

- Lower interest rates

- Flexible repayment terms

- Loan forgiveness options available

- Income-driven repayment plans

- No immediate repayment required

Disadvantages

- Long repayment periods (10-25 years)

- Interest accumulates during school

- Limited use (education only)

- Strict eligibility requirements

- May affect credit score

6. Credit Cards

Definition and Purpose

Credit cards are revolving lines of credit that allow you to borrow money up to a set limit and repay it over time. While technically not traditional loans, they function as short-term borrowing tools with high interest rates if balances aren’t paid in full monthly.

Key Features

- Revolving credit line

- Variable interest rates (typically 15-25% APR)

- Minimum monthly payments required

- Credit limit based on creditworthiness

- Rewards and benefits often included

Best For

- Everyday purchases

- Building credit history

- Emergencies

- Large purchases (with 0% promotional rates)

Advantages

- Convenient and accessible

- Build credit history

- Rewards and cashback

- Fraud protection

- Flexible repayment

Disadvantages

- Very high interest rates

- Easy to overspend

- Annual fees may apply

- Minimum payments don’t reduce principal quickly

- Debt can accumulate rapidly

7. Payday Loans

Definition and Purpose

Payday loans are short-term, high-interest loans designed to cover emergency expenses until the next paycheck. These loans are controversial due to their extremely high interest rates and predatory practices.

Key Features

- Short repayment term (typically 2 weeks)

- Small loan amounts ($300-$1,500)

- Extremely high interest rates (300-400% APR)

- Minimal credit requirements

- Quick approval and funding

Best For

- Emergency expenses only

- Last resort when other options unavailable

Advantages

- Quick approval

- Minimal requirements

- Fast funding

- No credit check

Disadvantages

- Extremely high interest rates

- Predatory lending practices

- Debt trap cycle

- Fees and penalties

- Illegal in some jurisdictions

8. Debt Consolidation Loans

Definition and Purpose

Debt consolidation loans combine multiple debts into a single loan with one monthly payment. These can be secured or unsecured and help simplify finances and potentially reduce interest rates.

Key Features

- Combines multiple debts

- Single monthly payment

- May offer lower interest rates

- Longer repayment terms

- Can be secured or unsecured

Best For

- Managing multiple debts

- Reducing interest rates

- Simplifying finances

- Improving credit score

Advantages

- Single payment simplifies finances

- May reduce overall interest

- Improves credit utilization ratio

- Predictable payments

- Faster debt payoff potential

Disadvantages

- May extend repayment period

- Total interest paid could increase

- Requires discipline to avoid re-accumulating debt

- May have origination fees

- Could hurt credit score initially

9. Home Equity Loans and Lines of Credit

Definition and Purpose

Home equity loans allow homeowners to borrow against the equity they’ve built in their property. These are secured loans with lower interest rates than unsecured loans.

Types

Home Equity Loans: Lump sum borrowed upfront with fixed payments.

Home Equity Lines of Credit (HELOC): Revolving credit line accessed as needed.

Key Features

- Secured by home equity

- Lower interest rates

- Tax-deductible interest (often)

- Flexible terms

- Large borrowing amounts possible

Best For

- Home improvements

- Debt consolidation

- Major expenses

- Business funding

Advantages

- Lower interest rates

- Tax-deductible interest

- Large borrowing amounts

- Flexible terms

- Builds wealth

Disadvantages

- Risk of losing home

- Requires home equity

- Longer approval process

- Closing costs required

- Variable rates possible (HELOC)

10. Peer-to-Peer Loans

Definition and Purpose

Peer-to-peer (P2P) loans connect borrowers directly with individual investors through online platforms. These loans offer an alternative to traditional banks with potentially better rates for some borrowers.

Key Features

- Online application process

- Quick approval and funding

- Rates based on creditworthiness

- Fixed terms and payments

- Unsecured loans

Best For

- Debt consolidation

- Personal expenses

- Those with fair credit

- Quick funding needs

Advantages

- Quick approval process

- Competitive rates

- Flexible terms

- Less stringent requirements than banks

- Online convenience

Disadvantages

- May have origination fees

- Interest rates vary widely

- Limited loan amounts

- Requires good credit for best rates

- Newer platform risk

Comparing Loan Types: Quick Reference Table

| Loan Type | Interest Rate | Collateral | Term | Best For |

|---|---|---|---|---|

| Personal | 6-36% | No | 2-7 years | General expenses |

| Secured | 3-15% | Yes | 2-10 years | Large purchases |

| Mortgage | 2-7% | Property | 15-30 years | Home purchase |

| Auto | 3-10% | Vehicle | 3-7 years | Vehicle purchase |

| Student | 3-8% | No | 10-25 years | Education |

| Credit Card | 15-25% | No | Variable | Daily purchases |

| Payday | 300-400% | No | 2 weeks | Emergency only |

| Debt Consolidation | 5-25% | Optional | 2-10 years | Multiple debts |

| Home Equity | 3-10% | Home | 5-20 years | Large expenses |

| P2P | 6-36% | No | 3-5 years | Debt consolidation |

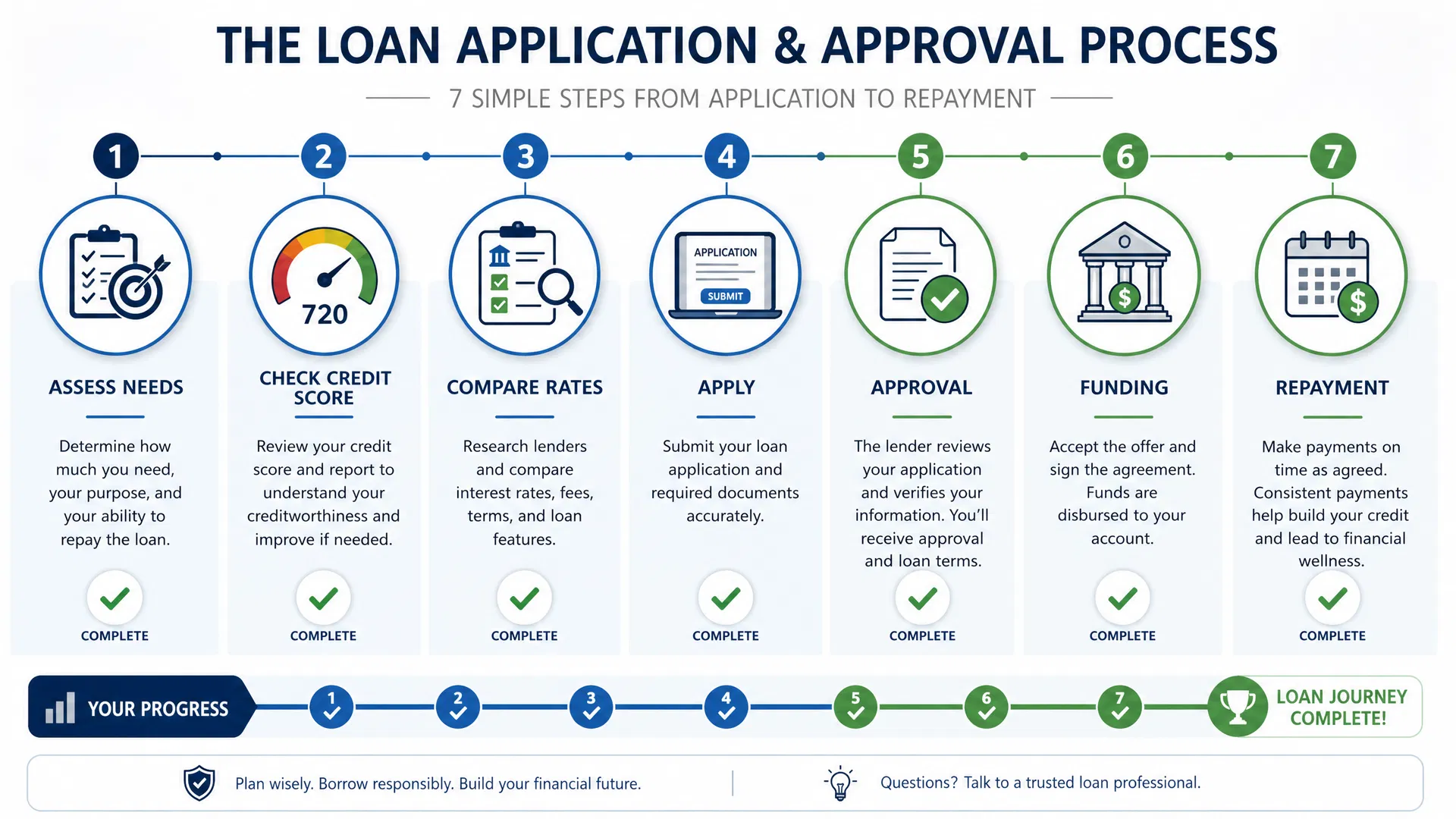

How to Choose the Right Loan Type

1. Assess Your Needs

Determine exactly what you need the money for and how much you need. Different loans serve different purposes, and choosing the right one depends on your specific situation.

2. Check Your Credit Score

Your credit score significantly impacts interest rates and approval chances. Review your credit report and understand your creditworthiness before applying.

3. Compare Interest Rates

Shop around with multiple lenders to find the best rates. Even small differences in interest rates can save you thousands over the life of the loan.

4. Review Terms and Conditions

Understand repayment periods, fees, penalties, and any other conditions before committing to a loan.

5. Calculate Total Cost

Don’t just look at interest rates; calculate the total amount you’ll pay including all fees and interest over the loan term.

6. Consider Your Financial Situation

Ensure monthly payments fit your budget and won’t strain your finances.

7. Avoid Predatory Lenders

Be cautious of extremely high interest rates and hidden fees. Research lenders carefully before applying.

Important Considerations

Conclusion

Understanding different loan types is essential for making informed financial decisions. Each loan type serves a specific purpose and comes with distinct advantages and disadvantages. Personal loans offer flexibility, mortgages provide wealth-building opportunities, and auto loans help you purchase vehicles at competitive rates. Meanwhile, payday loans should generally be avoided due to their predatory nature.

The key to successful borrowing is choosing the loan type that best matches your needs, financial situation, and ability to repay. Take time to compare options, understand the terms, and calculate the total cost before committing. By making an informed decision, you can access the funds you need while minimizing costs and protecting your financial future.

Remember to always read the fine print, ask questions, and seek professional advice when needed. Your financial health depends on making smart borrowing decisions today.

{kind=link}