Introduction

When you deposit money in a bank, you trust that your funds are safe. The Federal Deposit Insurance Corporation (FDIC) plays a crucial role in protecting that trust. FDIC insurance guarantees that your deposits are protected up to $250,000 per depositor, per insured bank, per account ownership category. This comprehensive guide explains how FDIC insurance works, what it covers, coverage limits, and how it protects your money in case of bank failure.

Understanding FDIC insurance is essential for anyone with bank accounts. Whether you’re opening your first savings account or managing multiple accounts, knowing your coverage limits ensures your money is properly protected.

What is FDIC Insurance?

The Federal Deposit Insurance Corporation (FDIC) is an independent agency created by Congress in 1933 to maintain stability and public confidence in the nation’s financial system. FDIC insurance protects depositors’ accounts at member banks if the bank fails. This protection is automatic—you don’t need to apply or sign up for FDIC insurance. If your bank is FDIC-insured, your eligible deposits are automatically covered.

The FDIC doesn’t require member banks to pay premiums directly to customers. Instead, member banks pay insurance premiums to the FDIC, which maintains a deposit insurance fund. This fund protects depositors when banks fail. Since the FDIC was created, no depositor has lost a penny of FDIC-insured deposits.

FDIC Coverage Limits Explained

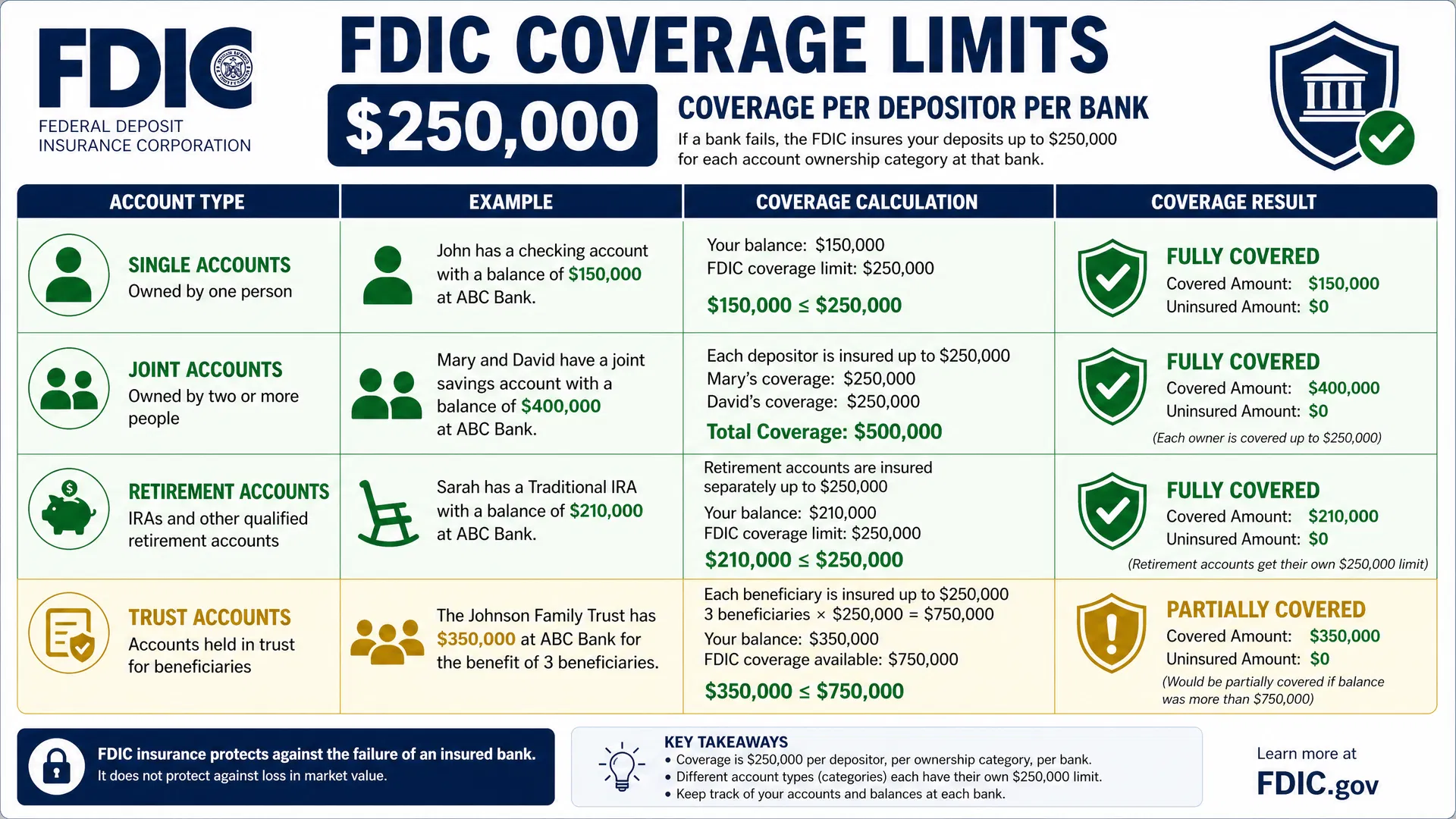

The standard FDIC coverage limit is $250,000 per depositor, per insured bank, per account ownership category. This means if you have $250,000 or less in a single account at one FDIC-insured bank, your entire balance is protected. If your balance exceeds $250,000, only the first $250,000 is covered.

Key Coverage Principles

- Per Depositor: Coverage applies to each individual depositor, not each account

- Per Insured Bank: Each bank’s coverage is separate. If you have accounts at multiple banks, each bank’s coverage is independent

- Per Ownership Category: Different account types (individual, joint, retirement) each have their own $250,000 coverage limit

Coverage Limits by Account Type

| Account Type | Coverage Limit | Description |

|---|---|---|

| Single Accounts | $250,000 | Accounts owned by one person |

| Joint Accounts | $250,000 per owner | Each co-owner gets separate $250,000 coverage |

| Retirement Accounts (IRA) | $250,000 | Traditional IRA, Roth IRA, SEP IRA, etc. |

| Trust Accounts | $250,000 per beneficiary | Coverage depends on number of beneficiaries |

| Payable-on-Death (POD) | $250,000 per beneficiary | Each beneficiary gets separate coverage |

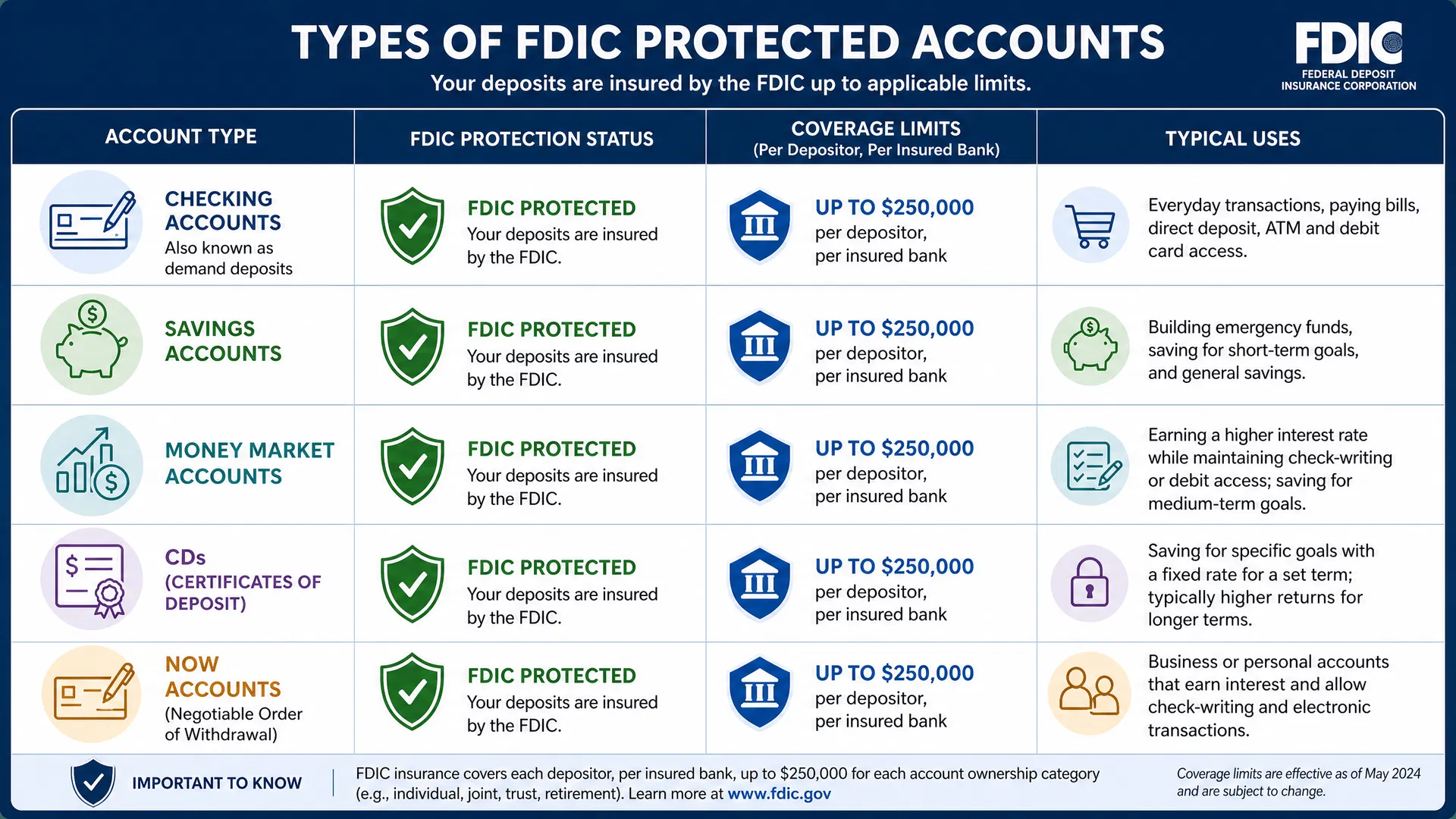

Types of FDIC Protected Accounts

Checking Accounts

Checking accounts are fully FDIC protected up to $250,000 per depositor, per bank. These accounts are designed for frequent transactions, paying bills, and everyday banking. Your checking account balance is automatically covered by FDIC insurance.

Savings Accounts

Savings accounts are FDIC protected up to $250,000 per depositor, per bank. These accounts are designed for building savings while earning interest. Many online banks offer high-yield savings accounts with competitive interest rates, and all deposits are FDIC protected.

Money Market Accounts

Money market accounts combine features of checking and savings accounts. They’re FDIC protected up to $250,000 per depositor, per bank. These accounts typically offer higher interest rates than regular savings accounts but may require larger minimum balances.

Certificates of Deposit (CDs)

CDs are time-deposit accounts where you agree to keep money deposited for a specific term (3 months to 5 years). CDs are FDIC protected up to $250,000 per depositor, per bank. Each CD is counted separately for coverage purposes if they have different maturity dates.

NOW Accounts

NOW (Negotiable Order of Withdrawal) accounts combine features of checking and savings accounts. They’re FDIC protected up to $250,000 per depositor, per bank. These accounts allow check-writing while earning interest.

What FDIC Insurance Does NOT Cover

FDIC insurance does not cover:

- Investment Products: Stocks, bonds, mutual funds, and other securities are not FDIC insured

- Safe Deposit Boxes: Contents of safe deposit boxes are not covered by FDIC insurance

- Brokerage Accounts: Even if held at an FDIC-insured bank, brokerage accounts are not FDIC insured

- Losses from Fraud or Theft: FDIC insurance covers bank failure, not personal fraud or theft

- Foreign Currency: Deposits in foreign currency are not covered

- Cryptocurrency: Digital assets and cryptocurrency are not FDIC insured

How FDIC Insurance Protects You When a Bank Fails

When an FDIC-insured bank fails, the FDIC takes several steps to protect depositors:

Step 1: Bank Closure

When a bank becomes insolvent (liabilities exceed assets), federal regulators close the bank and appoint the FDIC as receiver.

Step 2: FDIC Assessment

The FDIC assesses the bank’s condition, determines which deposits are insured, and calculates insurance payouts.

Step 3: Deposit Protection

The FDIC protects eligible deposits up to $250,000 per depositor, per account category. Deposits exceeding coverage limits may be recovered from the bank’s assets.

Step 4: Fund Distribution

Customers receive their insured funds through one of two methods: (1) Direct deposit to their account at another bank, or (2) Check mailed to their address. Typically, customers have access to their insured funds within 1-2 business days.

Historical Track Record

Since 1933, the FDIC has resolved over 500 bank failures. Throughout this history, no depositor has lost a penny of FDIC-insured deposits. This perfect track record demonstrates the strength and reliability of FDIC insurance.

Maximizing Your FDIC Coverage

Strategy 1: Use Multiple Banks

Since coverage is per bank, you can increase total coverage by spreading deposits across multiple FDIC-insured banks. For example, $500,000 split between two banks ($250,000 each) is fully covered, while $500,000 at one bank is only partially covered.

Strategy 2: Use Different Account Ownership Categories

Each account ownership category has separate $250,000 coverage. For example, you could have: (1) Individual account ($250,000), (2) Joint account with spouse ($250,000), (3) Retirement IRA ($250,000), (4) Trust account ($250,000 per beneficiary). This strategy allows families to protect much larger amounts.

Strategy 3: Understand Joint Account Coverage

Joint accounts receive special coverage treatment. Each co-owner is insured up to $250,000. A joint account with $500,000 ($250,000 per owner) is fully covered. However, if the account has three owners, each owner is insured up to $250,000, providing up to $750,000 total coverage.

Strategy 4: Verify Bank FDIC Status

Before depositing money, verify that your bank is FDIC-insured. Visit the FDIC’s Bank Find tool at www.fdic.gov or call 1-877-ASK-FDIC to confirm FDIC insurance status.

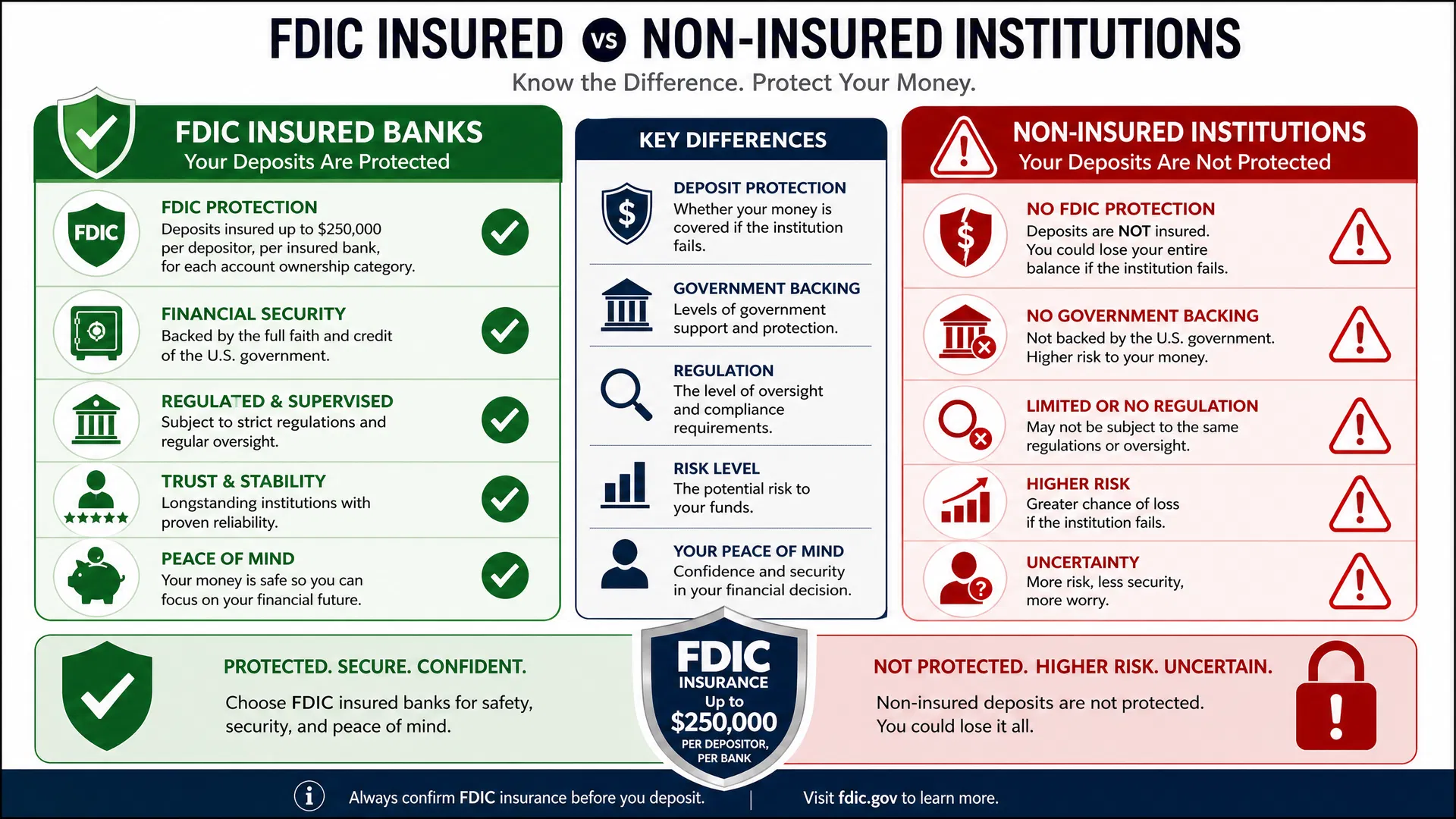

FDIC Insured vs. Non-Insured Institutions

Not all financial institutions are FDIC-insured. Understanding the difference is crucial for protecting your money.

FDIC-Insured Banks

FDIC-insured banks include most traditional banks and many online banks. These institutions are regulated by federal banking authorities and their deposits are protected by FDIC insurance. FDIC-insured banks display the FDIC logo and provide deposit insurance information.

Non-Insured Institutions

Non-insured institutions include some credit unions (insured by NCUA instead), money services businesses, and unregulated financial institutions. Deposits at non-insured institutions are not protected by FDIC insurance. If the institution fails, you could lose your entire deposit.

Frequently Asked Questions (FAQs)

A: FDIC insurance is automatic. If your bank is FDIC-insured, your eligible deposits are automatically covered. You don’t need to apply or pay for coverage.

A: Amounts exceeding $250,000 at one bank are not covered by FDIC insurance. To protect amounts over $250,000, spread deposits across multiple banks or use different account ownership categories.

A: No. FDIC insurance only covers deposit accounts (checking, savings, money market, CDs). Credit card balances are not covered. However, understanding credit card protections helps you manage credit responsibly.

A: Most online banks are FDIC-insured, but not all. Before opening an account, verify FDIC insurance status by checking the bank’s website or using the FDIC Bank Find tool.

A: Typically, FDIC-insured deposits are made available within 1-2 business days after a bank closes. In most cases, customers have access to their funds very quickly.

A: No. Savings bonds are not FDIC-insured. They’re backed by the U.S. government but through a different program, not FDIC insurance.

A: No. Multiple accounts at the same bank in the same ownership category are combined for coverage purposes. However, different ownership categories (individual, joint, retirement) each have separate $250,000 coverage.

A: Your debit card access may be temporarily interrupted, but your FDIC-insured deposits are protected. You’ll receive your funds through the FDIC’s resolution process.

People Also Asked Questions (PAA)

Common Questions People Search For

Yes, your money is safe in FDIC-insured banks. FDIC insurance protects deposits up to $250,000 per depositor, per bank. Since 1933, no depositor has lost a penny of FDIC-insured deposits. Banks are heavily regulated and audited to ensure financial stability.

Most traditional banks and many online banks are FDIC-insured. To verify FDIC insurance status, visit www.fdic.gov or use the FDIC Bank Find tool. Look for the FDIC logo on the bank’s website or in branches.

FDIC insurance protects up to $250,000 per depositor, per insured bank, per account ownership category. Joint accounts provide $250,000 coverage per owner. Retirement accounts are insured separately up to $250,000.

FDIC insurance does not cover: investment products (stocks, bonds, mutual funds), safe deposit box contents, brokerage accounts, losses from fraud or theft, foreign currency, or cryptocurrency. It only covers eligible deposit accounts.

No, credit unions are not FDIC-insured. Instead, they’re insured by the National Credit Union Administration (NCUA), which provides similar protection up to $250,000 per member, per credit union.

You cannot lose FDIC-insured deposits if your bank fails. However, you could lose money through fraud, unauthorized transactions, or by investing in non-FDIC-insured products like stocks or mutual funds.

Maximize FDIC coverage by: (1) Using multiple banks, (2) Using different account ownership categories, (3) Understanding joint account coverage, (4) Verifying FDIC insurance status. This strategy can protect significantly more than $250,000.

When an FDIC-insured bank fails, the FDIC takes control, assesses deposits, and distributes insured funds (up to $250,000 per depositor, per category) to customers within 1-2 business days. Uninsured amounts may be recovered from bank assets.

Important Considerations

Conclusion

FDIC insurance is a critical protection for bank depositors. Understanding how it works, what it covers, and coverage limits helps you protect your money effectively. The FDIC’s perfect track record since 1933 demonstrates the strength and reliability of this protection system.

By choosing FDIC-insured banks, understanding coverage limits, and using strategies to maximize protection, you can ensure your deposits are secure. Whether you’re saving for an emergency fund, building wealth, or managing retirement accounts, FDIC insurance provides peace of mind that your money is protected.

Remember: FDIC insurance is automatic at member banks, coverage is up to $250,000 per depositor per category, and you can maximize protection by using multiple banks and account types. Bank with confidence knowing your deposits are protected.

{kind=link}