Financial Goals for 2026: How to Set and Achieve Them

Setting financial goals is one of the most powerful steps you can take toward building wealth and achieving financial freedom. In 2026, with economic uncertainty and rising living costs, having clear financial goals provides direction, motivation, and a roadmap for making smart financial decisions. Whether you want to build an emergency fund, pay off debt, save for a house, or invest for retirement, this comprehensive guide will help you set meaningful goals and develop actionable strategies to achieve them.

Financial goals aren’t just about making more money—they’re about creating a life aligned with your values and priorities. This guide covers everything from understanding different types of goals to tracking progress and overcoming obstacles.

Complete guide to setting and achieving financial goals in 2026. Learn SMART goals framework, goal types, strategies, and how to stay motivated.

Why Financial Goals Matter

Financial goals provide structure and purpose to your money management. Without clear goals, it’s easy to spend money without intention, accumulate debt, and miss opportunities for wealth building. Goals help you prioritize spending, make better financial decisions, and track progress toward what matters most to you.

Research shows that people with written financial goals are significantly more likely to achieve financial success than those without goals. Goals create accountability, provide motivation during challenging times, and help you stay focused on long-term priorities rather than short-term temptations.

Understanding the SMART Goals Framework

The SMART framework is a proven method for setting goals that you can actually achieve. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound.

Specific

Your goal should be clear and specific, not vague. Instead of “save more money,” specify exactly what you’re saving for and how much. A specific goal might be “save $5,000 for an emergency fund” rather than “build savings.”

Measurable

You must be able to track progress toward your goal. Include numbers and metrics. “Reduce debt by $10,000” is measurable, while “pay off debt” is not. Measurable goals help you stay motivated by showing progress.

Achievable

Your goal should be realistic given your income, expenses, and circumstances. While ambitious goals are good, impossible goals lead to discouragement. Consider your financial situation and set goals you can realistically achieve with effort and discipline.

Relevant

Your goal should align with your values and long-term priorities. A goal is relevant if it matters to you and supports your bigger financial picture. Saving for something you don’t really want won’t motivate you.

Time-bound

Set a specific deadline for your goal. “Save $5,000 by June 2026” is time-bound, while “save $5,000 eventually” is not. Deadlines create urgency and help you stay focused.

Types of Financial Goals

Financial goals fall into three categories based on timeframe. Understanding these categories helps you balance immediate needs with long-term priorities.

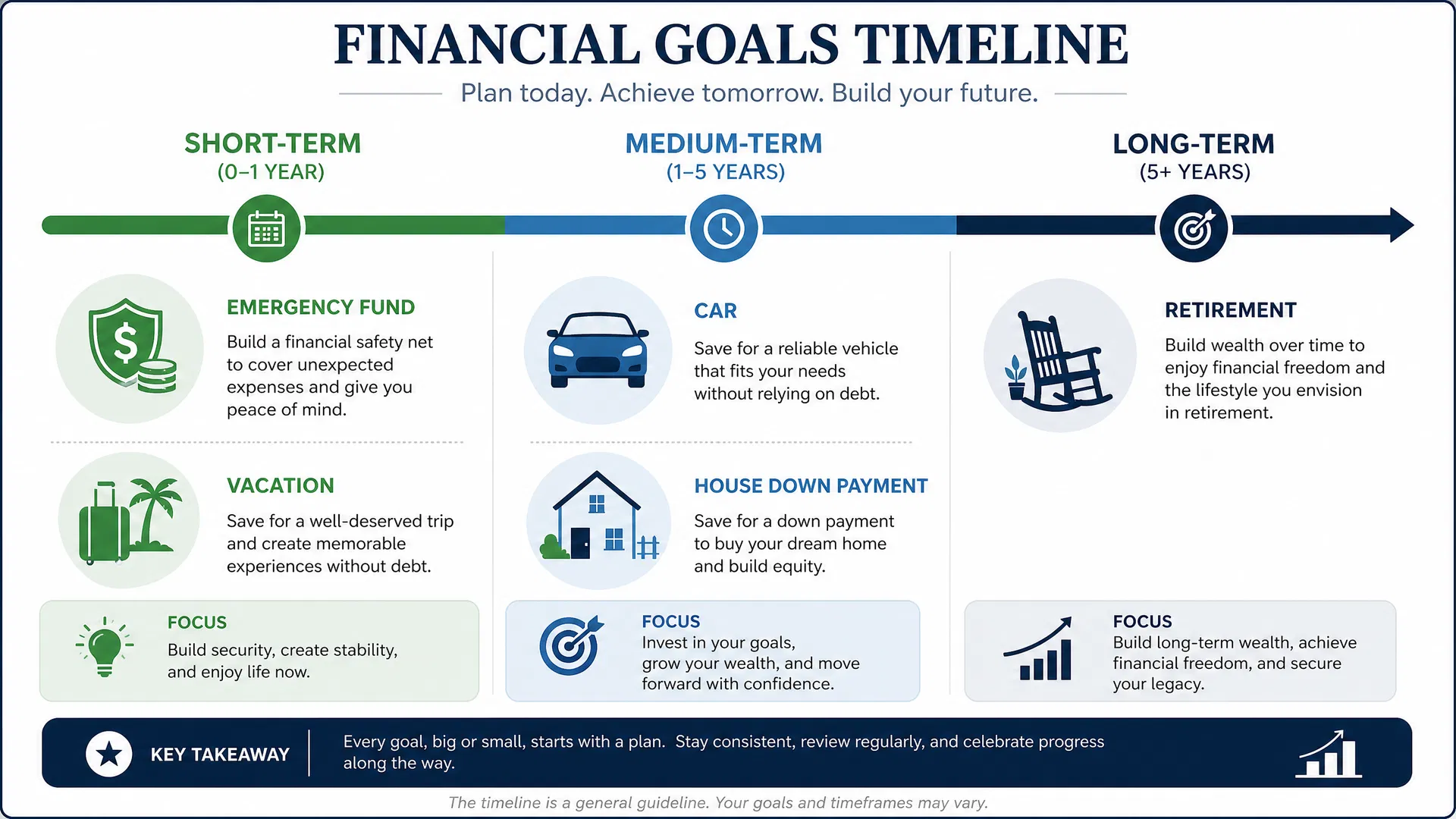

Short-Term Goals (0-1 Year)

Examples and Focus

Short-term goals include building an emergency fund, paying off credit card debt, saving for a vacation, or funding a planned purchase. These goals provide quick wins and build momentum. Focus on completing these goals to create positive financial habits and free up cash flow for medium and long-term goals.

Medium-Term Goals (1-5 Years)

Examples and Focus

Medium-term goals might include saving for a car down payment, building a larger emergency fund, paying off student loans, or saving for a house down payment. These goals require consistent effort and planning. Medium-term goals bridge the gap between immediate needs and long-term wealth building.

Long-Term Goals (5+ Years)

Examples and Focus

Long-term goals include retirement savings, college education funding, real estate investment, or building substantial wealth. These goals require patience, consistency, and often benefit from compound growth. Long-term goals provide the foundation for financial security and freedom.

Common Financial Goals for 2026

| Goal Type | Timeframe | Typical Amount | Monthly Savings | Why It Matters |

|---|---|---|---|---|

| Emergency Fund | 0-1 Year | $3,000-$10,000 | $250-$833 | Financial security and peace of mind |

| Debt Payoff | 1-3 Years | Varies | Varies | Reduce interest and improve credit |

| Vacation/Travel | 0-2 Years | $2,000-$5,000 | $83-$208 | Experiences and quality of life |

| Car Purchase | 1-3 Years | $5,000-$15,000 | $139-$417 | Transportation and independence |

| House Down Payment | 3-5 Years | $20,000-$50,000 | $333-$1,389 | Homeownership and wealth building |

| Retirement | 20-40 Years | $500,000+ | $500+ | Financial independence and security |

How to Set Your Financial Goals

Step 1: Assess Your Current Financial Situation

Before setting goals, understand where you stand financially. Calculate your net worth (assets minus liabilities), list all debts with interest rates, track your monthly income and expenses, and review your credit score. This honest assessment provides the foundation for realistic goal-setting.

Step 2: Identify Your Values and Priorities

What matters most to you? Is it financial security, experiences, family, education, or independence? Your goals should reflect your values. If family is important, prioritize goals like education savings or creating an emergency fund. If experiences matter, include travel savings.

Step 3: Write Down Your Goals

Write your goals using the SMART framework. Be specific, measurable, achievable, relevant, and time-bound. Writing goals increases commitment and makes them feel real. Keep your written goals visible—on your bathroom mirror, phone background, or journal.

Step 4: Prioritize Your Goals

You likely have multiple goals but limited resources. Prioritize based on importance and urgency. Generally, build an emergency fund first, then pay off high-interest debt, then work toward other goals. This order provides financial security and reduces financial stress.

Step 5: Create an Action Plan

For each goal, determine the specific actions needed. If your goal is “save $10,000 for a car down payment by December 2026,” your action plan might include: (1) open a dedicated savings account, (2) automate $833 monthly transfers, (3) reduce discretionary spending by $200/month, (4) find ways to earn extra income.

Strategies to Achieve Your Financial Goals

Automate Your Savings

Set up automatic transfers from your checking to savings account on payday. Automating removes temptation and ensures consistent progress. You can’t spend money that’s automatically moved to savings.

Track Your Progress

![]()

Monitor your progress regularly—monthly or quarterly. Seeing progress is motivating and helps you stay committed. Use spreadsheets, apps, or simple charts to visualize progress toward each goal.

Reduce Unnecessary Spending

Review your expenses and identify areas to cut. Small changes like reducing dining out, canceling unused subscriptions, or negotiating bills can free up hundreds monthly for goal achievement. Understanding credit card usage helps you avoid unnecessary interest charges that derail goals.

Increase Your Income

Consider side hustles, freelancing, or asking for a raise. Increasing income accelerates goal achievement. Even an extra $200-300 monthly significantly speeds progress toward financial goals.

Use the 50/30/20 Budget Rule

Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This framework ensures you’re consistently working toward goals while maintaining quality of life.

Your 2026 Financial Goals Roadmap

A comprehensive roadmap for 2026 might include: January-March (build emergency fund to $3,000), April-June (increase emergency fund to $6,000), July-September (pay down debt by $4,000), October-December (invest $2,000 and plan for 2027). Adjust this roadmap based on your specific goals and circumstances.

Overcoming Common Obstacles

Unexpected Expenses

Life happens. Car repairs, medical bills, and emergencies derail goals. Build a small emergency fund first to handle unexpected expenses without derailing other goals. This prevents using credit cards and accumulating debt.

Lack of Motivation

Long-term goals can feel overwhelming. Break them into smaller milestones and celebrate progress. Seeing progress toward short-term milestones keeps you motivated for long-term goals.

Income Instability

If your income varies, base goals on your lowest monthly income. This ensures you can always make progress even in lower-income months. During higher-income months, accelerate progress.

Lifestyle Inflation

As income increases, resist the urge to increase spending proportionally. Instead, direct increased income toward goals. This accelerates achievement and builds wealth faster.

Frequently Asked Questions (FAQs)

A: Most experts recommend 3-5 active goals at any time. Too many goals dilute focus and resources. Prioritize based on importance and urgency. Once you achieve a goal, add another.

A: Generally, build a small emergency fund ($1,000-$2,000) first, then focus on high-interest debt, then expand your emergency fund to 3-6 months of expenses. This approach prevents new debt from emergency expenses.

A: Aim to save 20% of your income for savings and debt repayment. If that’s not possible, start with 5-10% and increase gradually. Even small amounts add up over time.

A: Don’t give up. Adjust your goal timeline or amount if needed. Missing one month doesn’t mean failure. Recommit and get back on track. Progress over perfection is the goal.

A: Yes, if you have an emergency fund and manageable debt. Even small investments ($100-$200 monthly) benefit from compound growth over time. Start investing early for long-term wealth building.

A: Review goals monthly to track progress and quarterly to assess if goals still align with your priorities. Life changes, and goals should evolve accordingly.

A: Celebrate milestones, track progress visually, share goals with accountability partners, and remember your “why”—why these goals matter to you. Motivation comes from progress and purpose.

A: Yes, absolutely. Life circumstances change. If your situation improves, increase goals. If challenges arise, adjust timelines or amounts. Flexibility prevents discouragement while maintaining progress.

People Also Asked Questions (PAA)

Common Questions People Search For

Set realistic goals by assessing your current financial situation, considering your income and expenses, and using the SMART framework. Goals should be challenging but achievable. Research typical timelines and amounts for your goals. Consult with a financial advisor if needed.

Good beginner goals include: (1) Build $1,000 emergency fund, (2) Create a monthly budget, (3) Pay off credit card debt, (4) Start saving for a specific purchase, (5) Increase credit score by 50 points. Start with achievable goals to build confidence and momentum.

Start with $1,000 for small emergencies, then build to 3-6 months of living expenses. For most people, this means $5,000-$20,000. Calculate your monthly expenses and multiply by 3-6 to determine your target emergency fund.

Track goals using spreadsheets, budgeting apps, or simple charts. Review progress monthly. Visual tracking (progress bars, pie charts) is motivating. Many apps offer goal tracking features with automatic progress calculations.

Prioritize using the following order: (1) Emergency fund, (2) High-interest debt payoff, (3) Medium-term goals (car, vacation), (4) Long-term goals (retirement, house). This order provides security while building wealth.

Yes. Financial goals aren’t about the amount saved but consistency. On a low income, focus on small, achievable goals. Save even $25-50 monthly. Look for ways to increase income through side hustles. Every bit counts toward your goals.

Adjust your goals to be more realistic. Extend timelines, reduce target amounts, or focus on fewer goals. Alternatively, find ways to increase income or reduce expenses. Goals should motivate, not discourage. Make them achievable with effort.

Goals provide direction for consistent saving and investing. Consistent action over time builds wealth through compound growth. Goals also prevent wasteful spending and encourage smart financial decisions. Clear goals accelerate wealth building significantly.

Important Considerations

Conclusion

Setting and achieving financial goals is one of the most powerful steps toward financial freedom and peace of mind. By using the SMART framework, prioritizing goals, and implementing consistent strategies, you can achieve your financial dreams in 2026 and beyond.

Start today. Write down your goals, create your action plan, and take the first step. Remember, financial success is a journey, not a destination. Celebrate progress, stay consistent, and adjust as needed. Your financial future is built one goal at a time.

The best time to start was yesterday. The second-best time is today. Begin your financial goals journey now and watch your financial situation transform throughout 2026.

{kind=link}